Institutional Insights: Goldman Sachs 2026 Equity Outlook

2026 US Equity Outlook: Great Potential

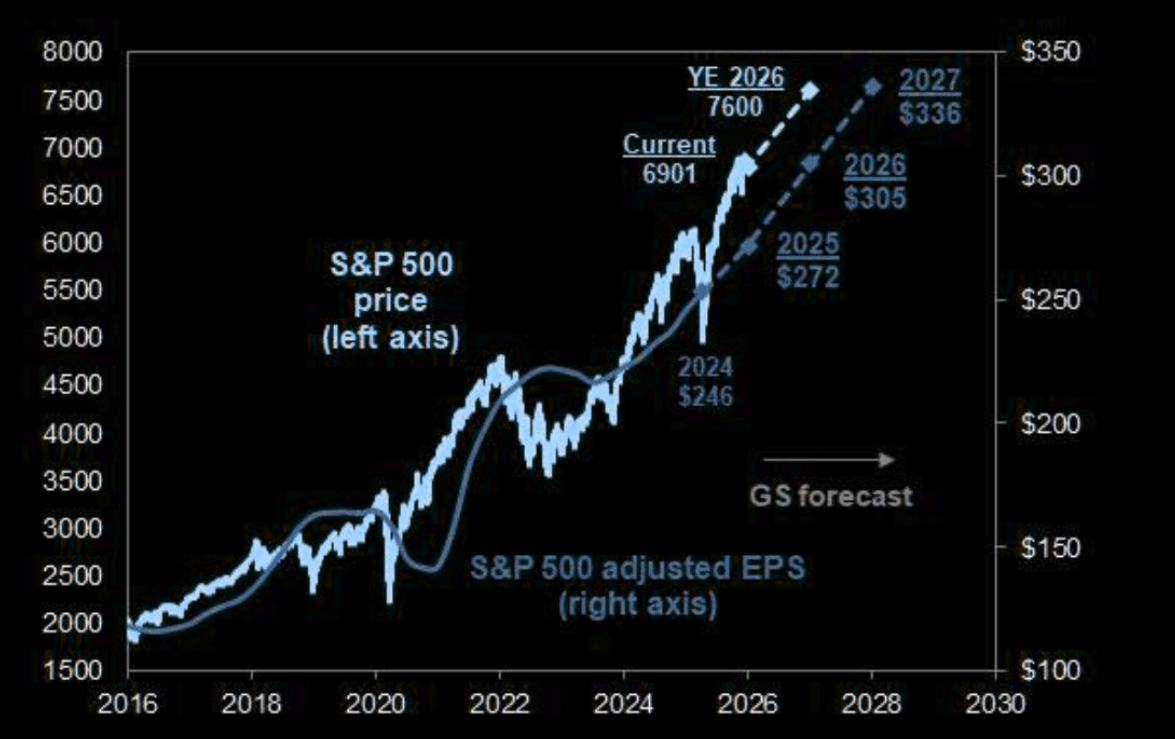

We anticipate another year of robust performance for U.S. equities in 2026, projecting a 12% total return for the S&P 500, reaching a year-end level of 7,600. Strong economic and revenue growth, sustained profit resilience among leading U.S. companies, and a productivity boost driven by AI adoption are expected to propel S&P 500 earnings per share (EPS) by 12% in 2026 and 10% in 2027, forming a solid foundation for the ongoing bull market.

While elevated valuations present the possibility of diverse outcomes, a catalyst is necessary to convert this potential energy into tangible equity gains. Our base case assumes a forward price-to-earnings (P/E) multiple of 22x on consensus EPS at the end of 2026, consistent with current levels and those projected for early 2025. Historical equity cycles suggest that the primary macro risks to the market are growth disappointments or interest rate shocks. However, our 2026 outlook, which includes healthy economic growth and continued Federal Reserve easing, typically supports rising valuation multiples.

The extreme concentration in equity markets and the evolving AI landscape are likely to drive sector rotations with broader market implications in 2026. The 10 largest stocks in the S&P 500 currently account for 41% of market capitalization and contributed 53% of the index's 2025 returns. While we expect AI spending to surpass consensus estimates, its growth rate may decelerate as corporate adoption increases. This dynamic could lead to rotations among major U.S. tech stocks, creating two-sided risks for the overall index.

As we enter 2026, investors have significant opportunities to capture both beta and alpha. For index investors, low implied volatility and tight credit spreads provide tools to capitalize on equity upside while mitigating downside risks. Meanwhile, a dynamic macroeconomic environment, wide valuation spreads, and low correlations present a fertile landscape for stock-pickers.

We identify five key investment themes for 2026:

1. Mid-Cycle Acceleration: Accelerating U.S. economic growth, coupled with easing monetary policy, is expected to boost cyclical sectors, particularly those tied to middle-income consumers and the nonresidential construction cycle, in early 2026.

2. The Great Re-Leveraging: Corporate leverage, while currently low, is expected to rise, with USD debt issuance likely exceeding $2 trillion. This trend will benefit companies in the lending ecosystem and favor stocks with strong free cash flow and a focus on shareholder returns.

3. The AI Future is Now: Corporate adoption of AI is set to increase, even as investment growth in the sector slows. The focus of the AI trade will likely shift from companies building AI infrastructure to those leveraging AI to enhance efficiency ("Phase 4") and those benefiting from AI-driven revenue growth ("Phase 3"). Additionally, attention will grow on "Phase 3-D," involving AI's integration with robotics and automation in the physical world.

4. The Art of the Comeback: A resurgence in IPO activity, increased M&A transactions, and continued equity market gains should drive a recovery in private equity exits, distributions, and fundraising. This will likely support a rebound in valuations for alternative asset managers after a volatile 2025.

5. The Search for Value: Wide valuation spreads and a supportive macroeconomic backdrop make Value an attractive factor in early 2026, following a surprisingly strong 2025. Sectors such as Health Care, Materials, Consumer Discretionary, and Software & Services stand out due to low valuations relative to historical levels and profitability, warranting an overweight recommendation.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!